$1M Warranty

Introducing the industry's first Card Testing Warranty for online businesses, designed to safeguard them from the growing threat of card testing.

Warranty Benefits

Real Impact, More Confidence, Better ROI

Arkose Titan effectively identifies and mitigates bots employed by fraudsters during card testing attacks. Our groundbreaking Card Testing Warranty safeguards up to $1 million in potential card authorization fee losses related to card testing incidents for Arkose Labs' managed service clients, provided Arkose Titan fails to prevent such an attack within the agreed-upon service level agreement.

We stand behind the efficacy of the platform in mitigating card testing attacks, which results in significant cost savings.

Covers the authorization processing fees resulting from card testing attacks costs up to $1m.

Legitimate consumers are never blocked and rarely experience user interdiction.

An effective security strategy that protects your customers, brand, and bottom line against card testing attacks.

Backed by top-tier insurance carrier and with our complete protection 24/7/365, you can enjoy cost savings without compromising your bottom line.

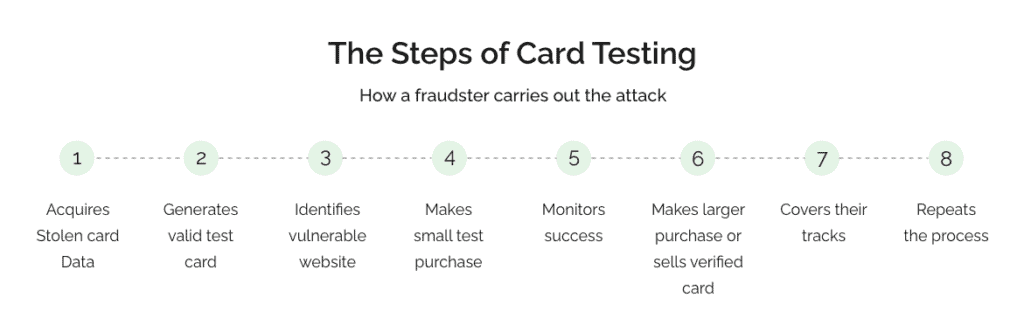

Card testing is a cyber threat where bad actors attempt to validate stolen or illicitly obtained payment card information by making small, unauthorized transactions or balance inquiries. These criminals usually obtain card details through methods like phishing, generation, or via black market repositories. They use card testing to validate elements such as the Issuer Identification Number (IIN), expiration date, and CVV before conducting fraudulent transactions.

We stand behind the efficacy of the platform in mitigating card testing attacks, which results in significant cost savings.

Covers the authorization processing fees resulting from card testing attacks costs up to $1m.

Legitimate consumers are never blocked and rarely experience user interdiction.

An effective security strategy that protects your customers, brand, and bottom line against card testing attacks

Backed by top-tier insurance carrier and with our complete protection 24/7/365, you can enjoy cost savings without compromising your bottom line.

Arkose stops fraud and digital abuse before it impacts your revenue. Trusted by Fortune 500 enterprises and top fintechs worldwide.

Stopping bots, AI agents, and fraud before they reach your users.